If you are a parent, it is likely that you have told your children that “patience is a virtue.” It is quite possible that you have reminded yourself of the merits to practice the art of patience when you are with your children as well. Patience, however, is also advantageous in many other situations. If you are an investor, patience can truly be a virtue. It can help you take advantage of opportunities that impatient investors may throw your way. It can also help minimize the costs associated with your portfolio, as holding on to stocks for longer periods, helps to minimize your tax burden and limit the frictional costs associated with investing. For those who are unfamiliar with the term, frictional costs refer to:

The costs associated with a trade such as part of the actual cost of the shares, broker commissions, exchange fees and the tax liability on any earnings. They can also include opportunity costs in terms of the research time spent identifying the security being purchased.

In the third edition of Robert Hagstrom’s book The Warren Buffett Way, Mr. Hagstrom added a chapter on the importance of patience in investing. In an interview on John Mihaljevic’s Value Investing Podcast, Mr. Hagstrom shared the results of some research related to the returns associated with various stock holding periods. The focus of the research was to determine, on average, how many stocks in the S&P 500 Index might double over a given time period. In looking at stock returns over the last 42-43 years, Mr. Hagstrom found the following: On average only 1.9% of the stocks in the S&P 500 (or eight-to-nine stocks) doubled over a 12-month period. Using rolling three-year periods, the study concluded that only 15%-16% (about 80 stocks) doubled in value. If the rolling time frame was extended to five years, then approximately 30% (or 150 equities) doubled.

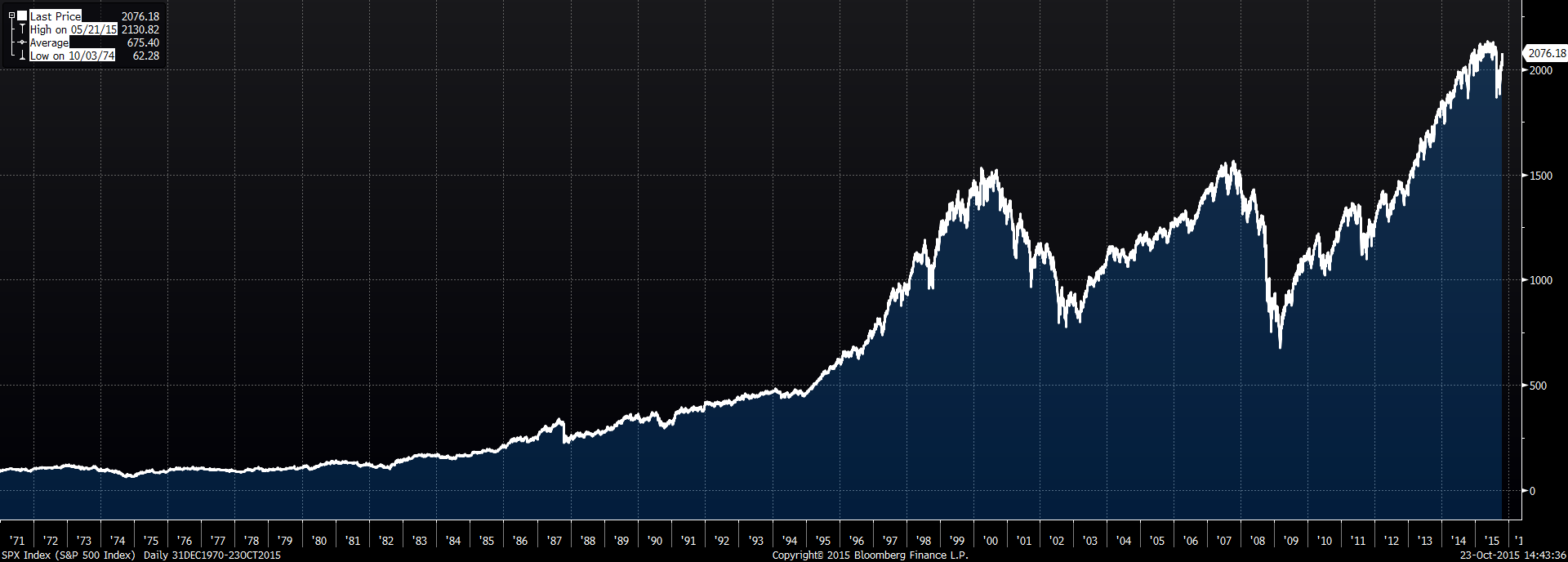

Five years might sound like a long time to wait for a stock to double. However, it really is not that long. That type of return also equates to a 14.9% annualized growth rate. Nearly every investor should be more than satisfied if she can earn 15% per year on her investments. The chart that appears below shows the performance of the S&P 500 over the last 45 years. It does not include dividends. Based on a starting value of 92.15 at the end of 1970, the S&P has generated annualized gains of 7.2%. If we include dividends, the total return would likely be around 9% per year. The 15% return investors can realize when a stock doubles over five years is double the gain of the S&P. In fact, based on our review of annual performance, the S&P 500 generated returns of more than 15% in only 16 of the 45 years (36%). Interestingly, the likelihood of the S&P rising 15% in a given year is only a little greater than the possibility of buying and holding a stock that doubles over a five-year period.

Performance of the S&P 500 from 1971-Present

While we profess that neither we nor anyone else can say with any degree of certainty what the market will do on a given day or over the short term in general, we remain committed to our view that over the long term, the market is likely to move higher. Although the market’s volatility appears to have tempered a bit recently, it certainly must have spooked some investors. According to data from the Investment Company Institute (ICI), investors pulled nearly $32 billion out of domestic equity mutual funds from August through mid-October. It is important to not to let emotions such as fear and greed impact how you manage your portfolio. At our weekly investment committee meetings, we regularly discuss the market and its performance. However, we try not to let it cloud our judgment. Instead, we remain steadfast in applying our investment approach and process.