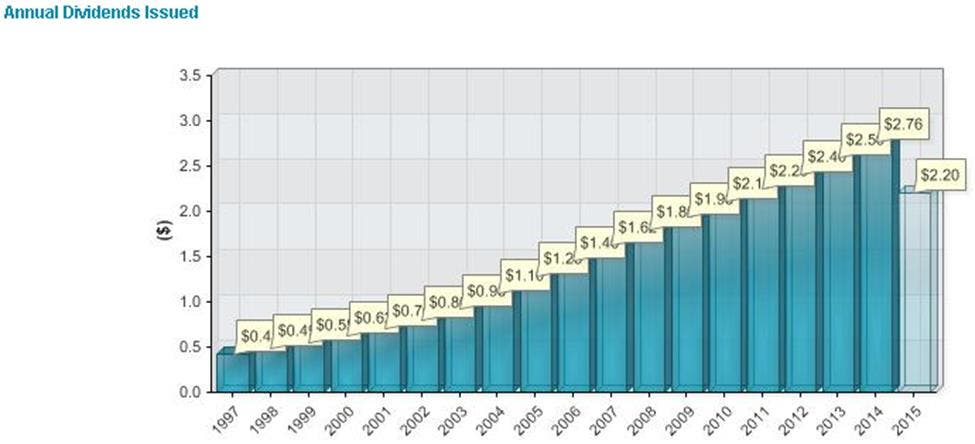

Dividend-paying stocks are an important part of client portfolios. We prefer companies with growing dividends. When companies regularly increase their dividends, the income earned from an investment relative to the purchase price (yield on cost) will rise. For example, last April Johnson & Johnson[i] (JNJ) increased its dividend for the 53rd consecutive year. (A chart showing the company’s dividend history since 1997 follows. JNJ has not yet declared its fourth quarter dividend. When it does, the total for the year should be $2.95.) If an investor purchased shares of JNJ in 2005 at that year’s average price of $64.72, her yield on those shares would have been 1.7%. If she still held those shares today, her yield on cost would be 4.6% ($2.95/$64.72).

Johnson & Johnson Annual Dividend History

Source: Johnson & Johnson company website: http://www.investor.jnj.com/divhistory.cfm

While companies will typically go to great lengths to protect their dividends, not every company has a dividend history like JNJ’s. The market typically reacts negatively when companies announce dividend cuts, so a dividend reduction is often the last step management will take when unexpected costs arise. The primary reasons a company might reduce its dividend are (1) financial stress and (2) unexpected expenses. There can be others, but the preceding are the main ones.

As part of our research process we evaluate the sustainability of a company’s dividend. Today, this issue is particularly relevant as lower oil prices have, in some cases materially impacted the cash flow of companies in the energy sector. Several companies have cut dividends, including operators of offshore rigs such as Seadrill, Transocean and Diamond Offshore. More recently, Denbury Resources, an exploration and production company, suspended its fourth quarter dividend. It seems likely more companies will reduce or eliminate their payouts.

National Oilwell Varco’s [i](NOV) customers include offshore drilling companies. Its business is also impacted by the activity level of Denbury and its peers. We thought it would be worth evaluating how safe NOV’s dividend might be.

To make a determination, we need to review NOV’s most recently filed quarterly financial statements or its 10-Q. Warning: This discussion will be technical. We start with the cash flow statement. In 2015’s first six months, NOV’s operating activities generated $308 million of cash flow. NOV’s capital expenditures (money invested in property plant and equipment) were $234 million. This means the company had free cash flow of $74 million ($308-$234). At June 30, NOV held $2.5 billion of cash and about $4.3 billion of interest-bearing debt. The cash interest paid on NOV’s deb t is comparatively low amounting to only $50 million over the last six months. Only $151 million of the company’s outstanding debt is classified as short-term (due in the next 12 months). The company also has $3.2 billion of available liquidity under its line of credit.

In 2015’s first half, the company’s dividend payments totaled $363 million. Based on the information presented, NOV should be able to continue paying its dividend. Its business is not consuming considerable cash, it has cash on its balance sheet and it has borrowing capacity.

However, we also note that NOV was a net borrower in the year’s first half. If we dig deeper, we see it spent nearly $1.8 billion on share repurchases. We have discussed share repurchases many times in the past (most recently in July), arguing that companies that allocate capital well should repurchase shares when they are undervalued not just when they have the cash. However, NOV has been borrowing to fund its buyback activity rather than using excess cash to fund it. Based on the data presented as well as the current environment, we think it more likely the company will pare back or eliminate its share repurchases and maintain its dividend.

There are many factors that have to be considered when evaluating the investment merits of individual securities. We know that dividends are an important component of investor returns. As part of our investment process, we evaluate a company’s potential to maintain and grow its dividend.

[i] Shares of Seadrill, Transocean, Ensco, Diamond Offshore, Denbury Resources and National Oilwell Varco are not currently part of BWFA’s “Buy/Hold” list.

[i] Shares of Johnson & Johnson are currently on BWFA’s “Buy/Hold” list, representing securities held in client portfolios.