Many clients have enviable cash balances in the bank, and if not, ample invested funds, to draw all at once to purchase large ticket items — homes, cars, boats.

In the past, those of us who are in any way attached to the “Great Depression ethic” from personal experience, or parents’ or grandparents’ influences, might automatically choose to pay cash. “I don’t want to owe anybody, anything!” “If I don’t have the money, I won’t buy!” These long held attitudes were born from a foregone era in very differing circumstances to today.

So, is paying cash automatically the better way to make these large purchases?

Many clients have discussed this very topic with us in recent months and years, and our answer still holds — NO, it is better to finance than pay cash for these large purchases.

DO NOT use investments to make large purchases – FINANCE.

DO NOT use cash in the bank to make large purchases – INVEST the cash, and FINANCE.

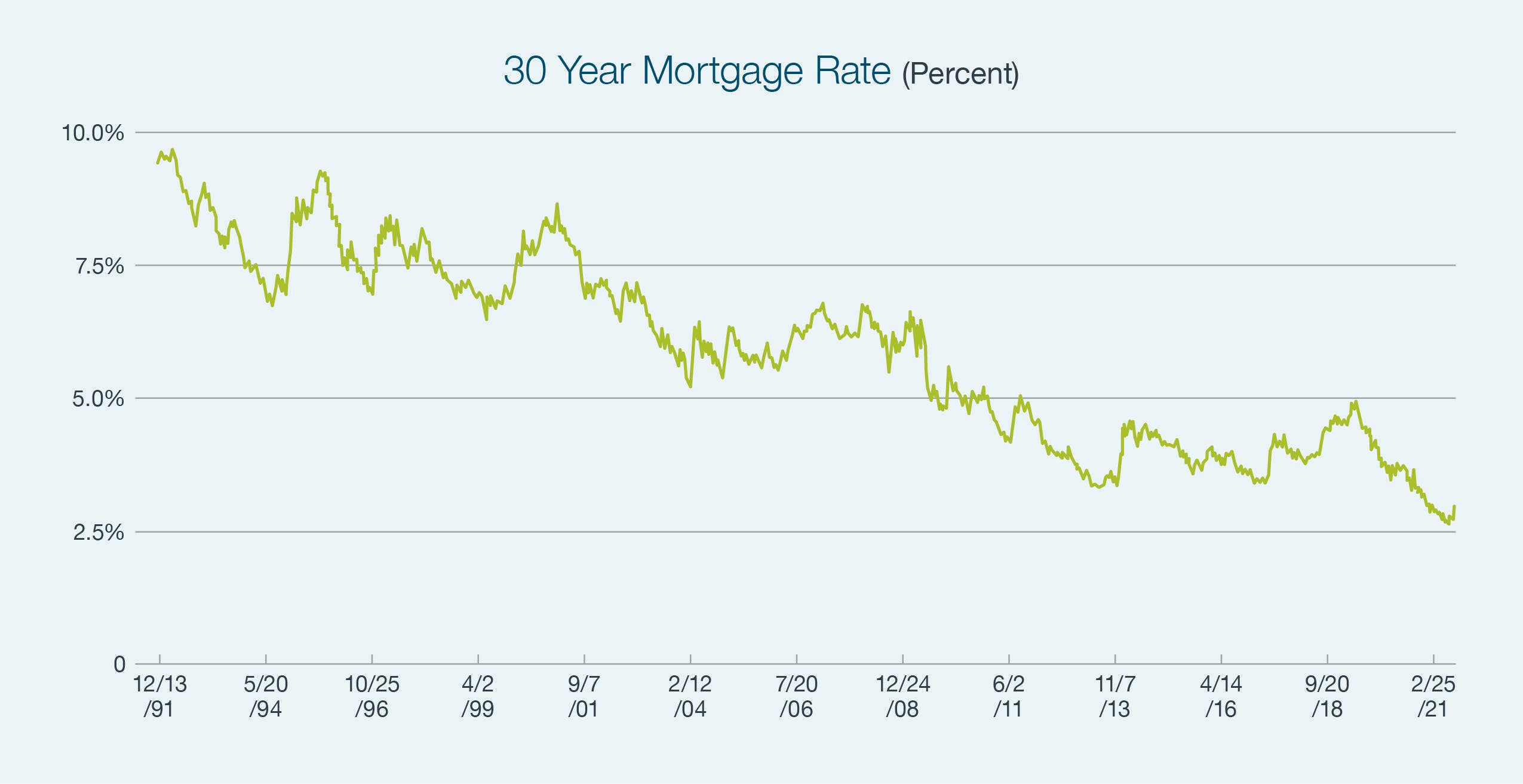

Given the downward trend in interest rates over the last several decades as illustrated in the chart, the cost of financing as compared to long-term annual returns on professionally managed portfolios, makes financing, versus using assets upfront, the clear decision today.

LET’S CONSIDER AN EXAMPLE

You purchase a vacation home for $500,000.

If you finance, you may put $100,000 down (and in some cases even less) and mortgage the remaining at 3% fixed rate (or lower, as of the writing of this article) for a full 30 years. The 30 year term keeps the payment low and maximizes the amount of years you borrow at this low rate.

Considering a conservative estimate of 7% investment portfolio return, per year on average, you will keep control of the $400,000 and take advantage of the opportunity to make 4% above the cost of the mortgage.

Using simple arithmetic, you stand to earn a net $16,000 ($400,000 multiplied by the net 4% your earn in this example) per year by keeping control of your portfolio funds.

Over a 30 year mortgage, that is additional investment earnings of $480,000! You may gradually draw down against this growing portfolio and additional earnings if you cannot pay the mortgage payment from regular current cash flow — salary, pensions, social securities, etc., but there is still large financial opportunity lost by buying with cash!

This simple calculation illustrates the point — finance, and keep your money invested — including large balances sitting idly in the bank.

Your 30 year potential net investment earnings in this example, will almost pay you back for the purchase price of the home!

Clients may not always choose the financing option.

Given the downward trend in interest rates over the last several decades as illustrated in the chart, the cost of financing as compared to long term annual returns on professionally managed portfolios, makes financing, versus using assets upfront, the clear decision today.

WHEN MIGHT YOU CONSIDER PAYING CASH UPFRONT?

- When rates go above 5% (not the case today)

- When you are just unwilling to invest your large cash bank balances but would use them to buy large items outright

- When you have a personal aversion to carrying debt

The first bullet will legitimately change the financial reasoning for financing, the next two bullets do not. You may be unwilling to finance in these low interest rate times, but the distinct financial benefit still exists.

So, with interest rates at historical lows, and when factoring in potential tax savings from deducting interest expense, and inflation, one is borrowing effectively for free! Why use you hard earned savings to make major purchases upfront in cash or to pay down debt early (assuming you are carrying low interest debt)? Invest all your available funds and borrow for your house or car or boat — that is the prudent choice!

Are you worried about borrowing in retirement or on a fixed income? Do you just want to learn more? Ask a BWFA advisor for guidance. We have resources to assist with various lending options and we can more specifically review the impact to your overall financial plan.

JOSEPH MANFREDI

MBA

COO, Senior Portfolio Manager & Executive Manager

jmanfredi@bwfa.com