If you participate in a 401(k), ESOP, or other qualified retirement plan that lets you invest in your employer’s stock, you need to know about net unrealized appreciation — a simple tax deferral opportunity with an unfortunately complicated name.

When you receive a distribution from your employer’s retirement plan, the distribution is generally taxable to you at ordinary income tax rates. A common way of avoiding immediate taxation is to make a tax-free rollover to a traditional IRA. However, when you ultimately receive distributions from the IRA, they’ll also be taxed at ordinary income tax rates. (Special rules apply to Roth and other after-tax contributions that are generally tax-free when distributed.)

But if your distribution includes employer stock (or other employer securities), you may have another option — you may be able to defer paying tax on the portion of your distribution that represents net unrealized appreciation (NUA).

You won’t be taxed on the NUA until you sell the stock. What’s more, the NUA will be taxed at long-term capital gains rates — typically much lower than ordinary income tax rates. This strategy can often result in significant tax savings.

WHAT IS NET UNREALIZED APPRECIATION?

A distribution of employer stock consists of two parts: (1) the cost basis (that is, the value of the stock when it was contributed to, or purchased by, your plan), and (2) any increase in value over the cost basis until the date the stock is distributed to you. This increase in value over basis, fixed at the time the stock is distributed in-kind to you, is the NUA.

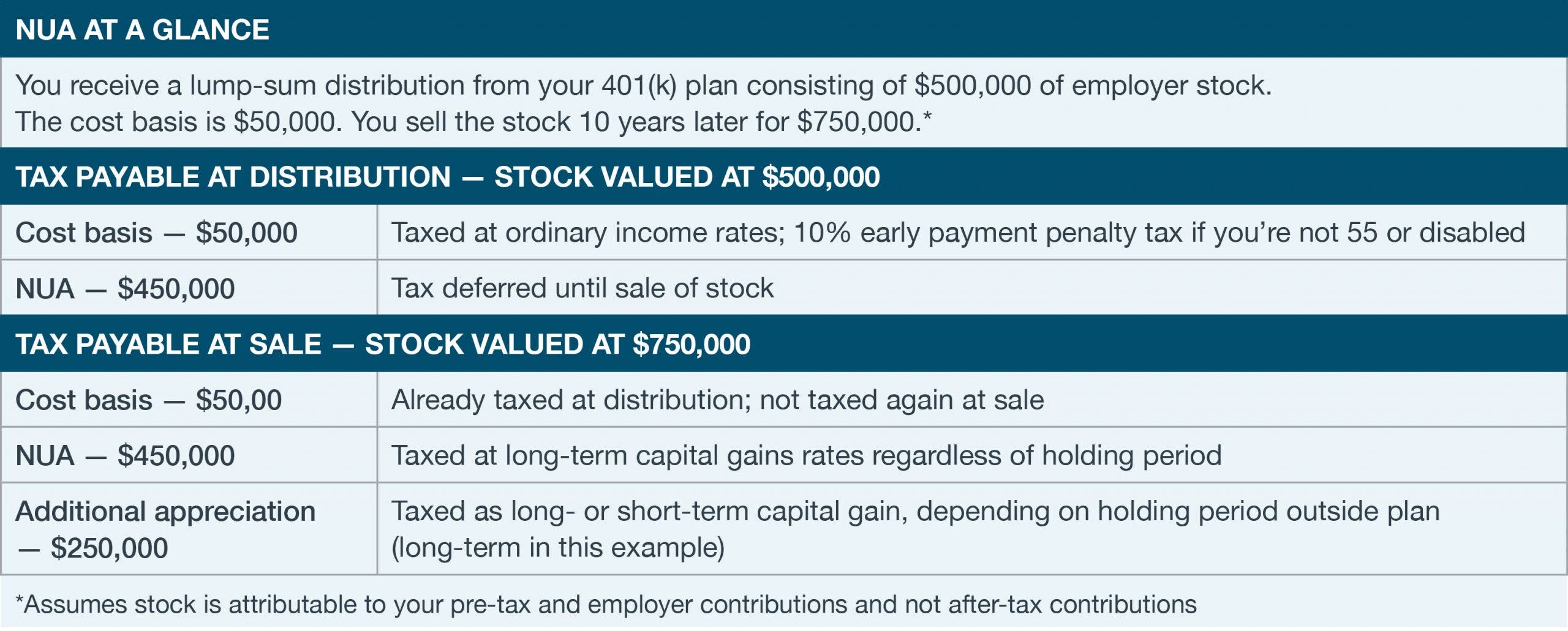

For example, assume you retire and receive a distribution of employer stock worth $500,000 from your 401(k) plan, and that the cost basis in the stock is $50,000. The $450,000 gain is NUA.

HOW DOES IT WORK?

At the time you receive a lump-sum distribution that includes employer stock, you’ll pay ordinary income tax only on the cost basis in the employer securities. You won’t pay any tax on the NUA until you sell the securities. At that time the NUA is taxed at long-term capital gain rates, no matter how long you’ve held the securities outside of the plan (even if only for a single day). Any appreciation at the time of sale in excess of your NUA is taxed as either short-term or long-term capital gain, depending on how long you’ve held the stock outside the plan.

Using the example on page 10, you would pay ordinary income tax on $50,000, the cost basis, when you receive your distribution. Let’s say you sell the stock after ten years, when it’s worth $750,000. At that time, you’ll pay long-term capital gains tax on your NUA ($450,000). You’ll also pay long-term capital gains tax on the additional appreciation ($250,000), since you held the stock for more than one year. Note that since you’ve already paid tax on the $50,000 cost basis, you won’t pay tax on that amount again when you sell the stock.

If your distribution includes cash in addition to the stock, you can either roll the cash over to an IRA or take it as a taxable distribution. And you don’t have to use the NUA strategy for all of your employer stock — you can roll a portion over to an IRA and apply NUA tax treatment to the rest.

In general, the NUA strategy makes the most sense for individuals who have a large amount of NUA and a relatively small cost basis. However, whether it’s right for you depends on many variables, including your age, your estate planning goals, and anticipated tax rates.

WHAT IS A LUMP-SUM DISTRIBUTION?

In general, you’re allowed to use these favorable NUA tax rules only if you receive the employer securities as part of a lump-sum distribution.

To qualify as a lump-sum distribution, both of the following conditions must be satisfied:

- It must be a distribution of your entire balance, within a single tax year, from all of your employer’s qualified plans of the same type (that is, all pension plans, all profit-sharing plans, or all stock bonus plans)

- The distribution must be paid after you reach age 59½, or as a result of your separation from service, or after your death

NUA IS FOR BENEFICIARIES, TOO

If you die while you still hold employer securities in your retirement plan, your plan beneficiary can also use the NUA tax strategy if he or she receives a lump-sum distribution from the plan. The taxation is generally the same as if you had received the distribution. (The stock doesn’t receive a step-up in basis, even though your beneficiary receives it as a result of your death.)

If you’ve already received a distribution of employer stock, elected NUA tax treatment, and die before you sell the stock, your heir will have to pay long-term capital gains tax on the NUA when he or she sells the stock. However, any appreciation as of the date of your death in excess of NUA will forever escape taxation because, in this case, the stock will receive a step-up in basis.

Using our example, if you die when your employer stock is worth $750,000, your heir will receive a step-up in basis for the $250,000 appreciation in excess of NUA at the time of your death. If your heir later sells the stock for $900,000, he or she will pay long-term capital gains tax on the $450,000 of NUA, as well as capital gains tax on any appreciation since your death ($150,000). The $250,000 of appreciation in excess of NUA as of your date of death will be tax-free.

SOME ADDITIONAL CONSIDERATIONS

- If you want to take advantage of NUA treatment, make sure you don’t roll the stock over to an IRA. That will be irrevocable, and you’ll forever lose the NUA tax opportunity.

- You can elect not to use the NUA option. In this case, the NUA will be subject to ordinary income tax (and a potential 10% early distribution penalty) at the time you receive the distribution.

- Holding a significant amount of employer stock may not be appropriate for everyone. In some cases, it may make sense to diversify your investments.

WHEN IS IT THE BEST CHOICE?

In general, the NUA strategy makes the most sense for individuals who have a large amount of NUA and a relatively small cost basis. However, whether it’s right for you depends on many variables, including your age, your estate planning goals, and anticipated tax rates. In some cases, rolling your distribution over to an IRA may be the better choice.

CHRIS KELLY

CPA, CFP®, M. ACCY

Financial Advisor, Portfolio Manager & Executive Manager

ckelly@bwfa.com