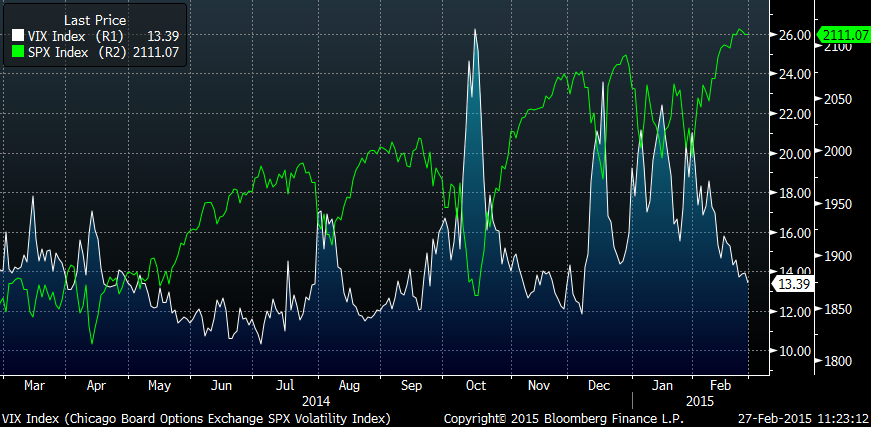

Over the last six months, equity markets have become more volatile. The VIX, which is the Chicago Board Options Exchange’s widely followed measure of volatility on the S&P 500, spiked several times in January. As shown in the below chart (the S&P 500 is represented by the green line, the VIX by the white line), over the past year, volatility increases when the S&P 500 falls and decreases as the market rises. Similar results can be seen for longer periods.

It should not be surprising to see volatility rise when the market declines. Falling markets are often driven by greater uncertainty. Investors become less confident that the market will rise, making them more likely to reduce their allocations to the market. This tendency is likely driven by the financial media, as the messages of market bears grow loudest when performance weakens.

In general, the accepted view is that higher volatility reflects higher risk. However, the harder question to answer is: how much or how real is the risk? If we review history, we will note that volatility spikes around recessions as it did in 2008. At the same time, it also peaks during periods of economic stress. The volatility spike this past October was at least partly driven by Ebola-related fears. This latter example turned out to be relatively insignificant.

In part, it is hard to tell what volatility means because it is driven by so many uncertain data points. It can be hard to distinguish between true information and noise. Even if you only occasionally glance at the financial headlines, it should be pretty clear that there is a lot of market noise these days. One reason for this is that the media gets paid to chatter, and that chatter is used as a means to attract viewers. Over time, we have become much more plugged in and our access to the news on a real-time basis has increased. This often leaves investors with more information, and more opinion and analysis about what that information might mean than they can effectively process.

On the geopolitical front, the news may be good one day, and uncertain or outright bad the next. The U.S. economy is performing well. On the other hand, times seem a bit tougher in Europe, Japan and many countries in the developing or emerging world. There is uncertainty about the situation in Russia; growth in China has slowed.

There are also the crude oil markets to consider. Production has increased. Prices have fallen more than 50% from their levels of last summer. One day a report may come out saying that it is “business-as-usual” for oil markets. The next an analyst may forecast that oil prices still have much farther to fall.

Even central banks are behaving differently due to differences in their economic environment. The U.S. is contemplating a rate hike. In Europe, quantitative easing (QE) is just starting. In Japan, QE is ongoing.

At BWFA, we do our best to tune out the noise. We view volatility as opportunity. When shares of a well-managed company fall, we look to see if the price decline presents opportunity. The difference between the 52-week high and the 52-week low price for many companies is far too wide (https://www.bwfa.com/articles/long-term-investing-still-works/). As a general rule, a company’s fundamental value does not change by tens of billions of dollars in a single year. Sometimes price declines are justified; however, there are also times when the market clearly overreacts to uncertainty. These events and situations create ideal opportunities for investors with a long-term focus.