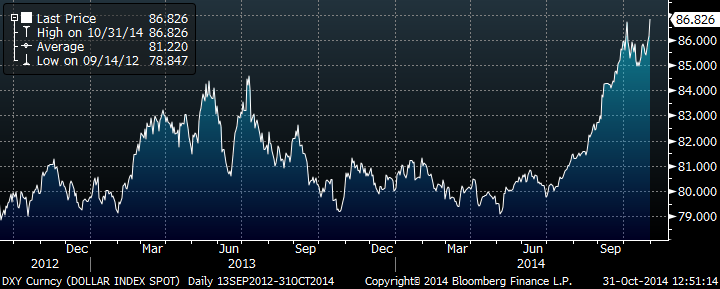

On Wednesday, the Fed ended the third round of Quantitative Easing (QE3). At its inception in September 2012, many were critical of the policy, fearing it would lead to higher inflation and a weaker dollar. As can be seen from the chart that appears directly below, the dollar actually strengthened while QE3 was in effect. This result reminds us once again of the perils of forecasting. There are many market pundits. They are rarely held accountable; they are frequently incorrect.

US Dollar Index (indicates general international value of the US Dollar versus major currencies commencing 09/13/2012).

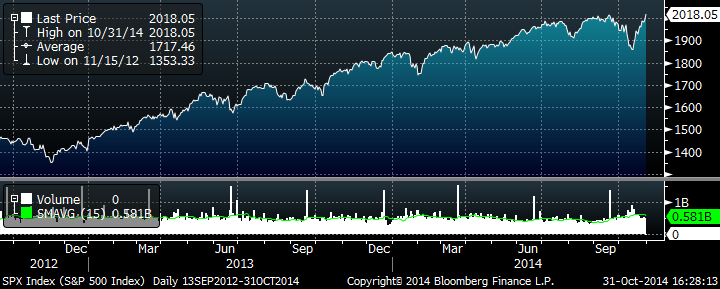

Unemployment fell from 8.1% when QE3 began to 5.9% when it ended. While the economy has not grown at the pace that is typically expected during an economic expansion, GDP has moved steadily higher. For investors, QE3 has been a boon, as the S&P 500 Index delivered superior returns. In fact, it is up nearly 50% from its lows of November 2012.

S&P 500 Index Performance commencing 09/13/2012.

The question for investors is what happens next. U.S. labor market conditions have improved, the U.S. economy continues to grow (preliminary data show a 3.5% increase in third-quarter GDP) and inflation has been relatively benign. Unfortunately, the environment in the rest of the world is not as strong. There are continued concerns about Europe and Japan, and growth in developing countries such as China has slowed. In fact, the U.S. economy is typically viewed as the bright spot globally.

At some point, the Fed is expected to raise rates. The language in the statement released after the latest Federal Reserve meeting still includes its “considerable time” language. This refers to when the Fed believes it may begin to raise rates. However, the statement has been qualified to emphasize that any decision to raise rates will depend on the economy’s health.

Most observers expect the first rate increase in 2015’s second quarter. At the same time, the more important question could be how fast rates may rise. To a large extent, the pace of interest rate increases will be dependent on the performance of the economy, the inflation outlook and the financial markets. The one thing the Fed probably wants to avoid most is the need to start QE4.

When the Fed does begin raising rates, its actions will show confidence that economic growth is on a sustainable path. As long as higher interest rates do not create financial market turmoil, we should expect a gradual normalization of monetary policy with a series of small rate hikes. On the other hand, if the financial markets overreact, some posit a once-and-done scenario where the Fed raises rates once and then stops.

The decision to end QE3 was expected. The U.S. economy continues to expand and, relative to the rest of the world, is probably best positioned for near-term growth. We believe the backdrop remains positive for stocks. While the S&P 500 Index has recovered from its mid-October lows, there are still some stocks that have not. We are looking for opportunities to purchase such securities at attractive prices, as we believe they can benefit long-term returns in client portfolios.