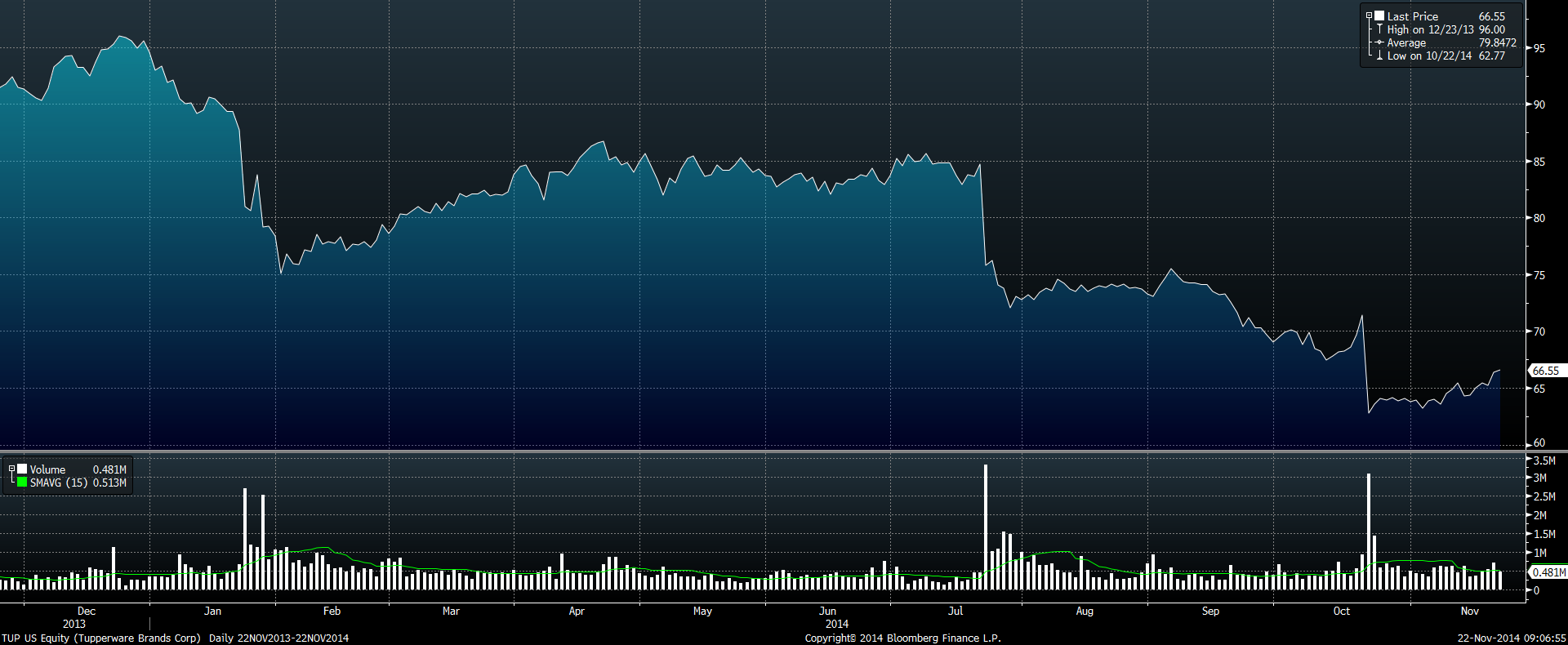

A recent search for a stock paying a solid dividend that could be added to client portfolios led us to take Tupperware Brands Corporation (TUP) through our investment process. As depicted below, the shares have underperformed over the past year. This decline could represent an opportunity. TUP also pays a strong dividend and looks to be trading at an attractive valuation.

For most, TUP no longer comes to mind as readily as it once did as Tupperware parties in the U.S. are no longer as popular as they once were. Given the apparent attractiveness of the valuation, as well as the strong dividend yield, we decided to undertake further analysis to assess TUP’s worthiness as a potential investment.

Our research showed that the company is much different than we remembered. While management says a Tupperware party takes place somewhere in the world every 1.3 seconds, the parties are mostly outside the U.S. In fact, roughly 90% of TUP’s revenues are generated internationally. Even more surprising is that roughly two-thirds of sales are in emerging markets. This is particularly intriguing from an investment perspective, as the increasing number of people living in these countries can ultimately benefit the size of TUP’s potential market. As these countries become more affluent, their middle class population should also increase.

Interestingly, TUP is viewed as helping to empower women in many of its markets. In many emerging markets, there are very limited earning opportunities for women. TUP can provide these women with the chance to start their own businesses. We like this element and the strong emerging market presence.

Our analysis of TUP also identified some concerns. The company’s direct sales force has declined in size on a year-over-year basis for 10 consecutive quarters. This is a possible issue, as TUP relies on a direct-to-consumer sales model. Additionally, disappointing performance of TUP’s shares this year has likely been caused by a growth outlook that has continued to weaken as the year has progressed. The U.S. dollar’s strength has also negatively impacted results, as foreign currency sales translate into fewer U.S. dollars. There are also reasons to believe that TUP could be underestimating the need to invest in the business. Higher promotional spending in Europe (particularly Germany) was one of the drivers behind TUP’s weaker fourth-quarter earnings guidance – the higher spending will increase expenses and reduce earnings. Finally, TUP carries more debt on its balance sheet than we would like. This can make it harder for it to manage the current downturn in its performance. We also think it increases the risk of a dividend cut if results do not improve in the next year or so.

Ultimately, we decided to pass on investing in TUP shares for now. We will, however, keep tracking their performance. There could be a better time to invest in the future. We would like to see some signs of improvement in the business performance before establishing a position, as we are concerned that continued weak performance could make TUP a value “trap” rather than a value.