The income provided by dividend-paying stocks can be a critical element of long-term returns. First, dividends always represent positive returns. As dividends rise, the related investment income increases. For retirees, a strong stream of dividend payments can reduce the need to sell assets to meet spending needs and make it a little easier to navigate the stock market’s ups and downs. Companies typically only cut their dividends when management believes they have little choice but to do so. As a result, the dividend income earned from most investments is likely to increase over time.

When looking at the yield a stock provides, investors most commonly look at its current dividend and compare it to the share price. For example, if you invest $10,000 today in a stock paying a total annual dividend of $200.00, then the stock’s yield is 2%. However, dividends are unlikely to remain constant year after year. Instead, many companies strive to increase them annually.

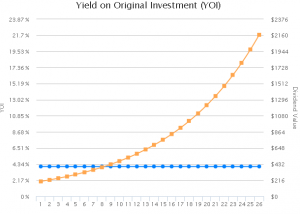

This is where a concept that can be referred to as yield on original investment (YOI) comes into play. Based on the preceding example, in seven years the dividend will increase from $2.00 to $3.90. Let us also assume that the value of the investment doubles over this period to $20,000. The current yield on the shares will be 1.95% ($3.90/$200). However, the YOI will be 3.9% ($3.90/$100). If the average dividend increase is 10% over a 14-year period, the dividend will grow to $7.59 per share, representing a YOI of 7.59%.

We can also compare this investment to a bond. If we buy bonds paying investors 4% annually, the income earned from the bonds will be $400 per year for as long as the bonds are outstanding. Initially, the bonds will generate more income than the shares of stock noted above. However, over time, the situation will change. The following chart was derived using a future income-yield calculation tool developed by Miller/Howard Investments, a boutique investment manager. It shows that in year eight, the annual income from the dividend-paying stock will be greater than that provided by the bonds. If the annual increase to the stock’s dividend can increase by 10%, on average over 26 years, the YOI will increase to 21.67% or $2,167. The bond will still pay only $400 that year. In fact, the bond would provide $10,400 over the entire 26-year period. Beginning in year 19, the stock will pay more in annual dividends than the bond will pay over the entire period.

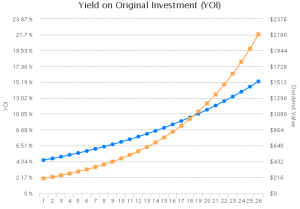

It may also be instructive to compare a stock with a higher yield and a slower growth rate to one with a lower yield and a higher growth rate. For example, we can compare a stock currently yielding 4.5% with expected annual dividend increases of 5% to a stock currently yielding 2% for which 10% annual dividend increases are expected. In this case, it will take 19 years until the annual dividend paid by the stock with the lower current yield will surpass that of the stock with the higher current yield.

We know that real-life scenarios may not play out as cleanly as the ones discussed here. At the same time, they point out the value provided by a dividend that increases over time. They also remind us of the value a higher initial yield plays in generating a high future YOI. One can also question whether or not the faster grower would be able to sustain the type of growth outlined here. The more time that goes on and the bigger a company gets, the harder it is to sustain these types of results.

This discussion is not meant to say that bonds (or bond funds) should not be included in a diversified portfolio. They should. But, the examples above also demonstrate the value of a dividend that increases over time. We favor stocks with the potential to increase their dividend over time to those that are more likely to maintain their dividend closer to current levels.