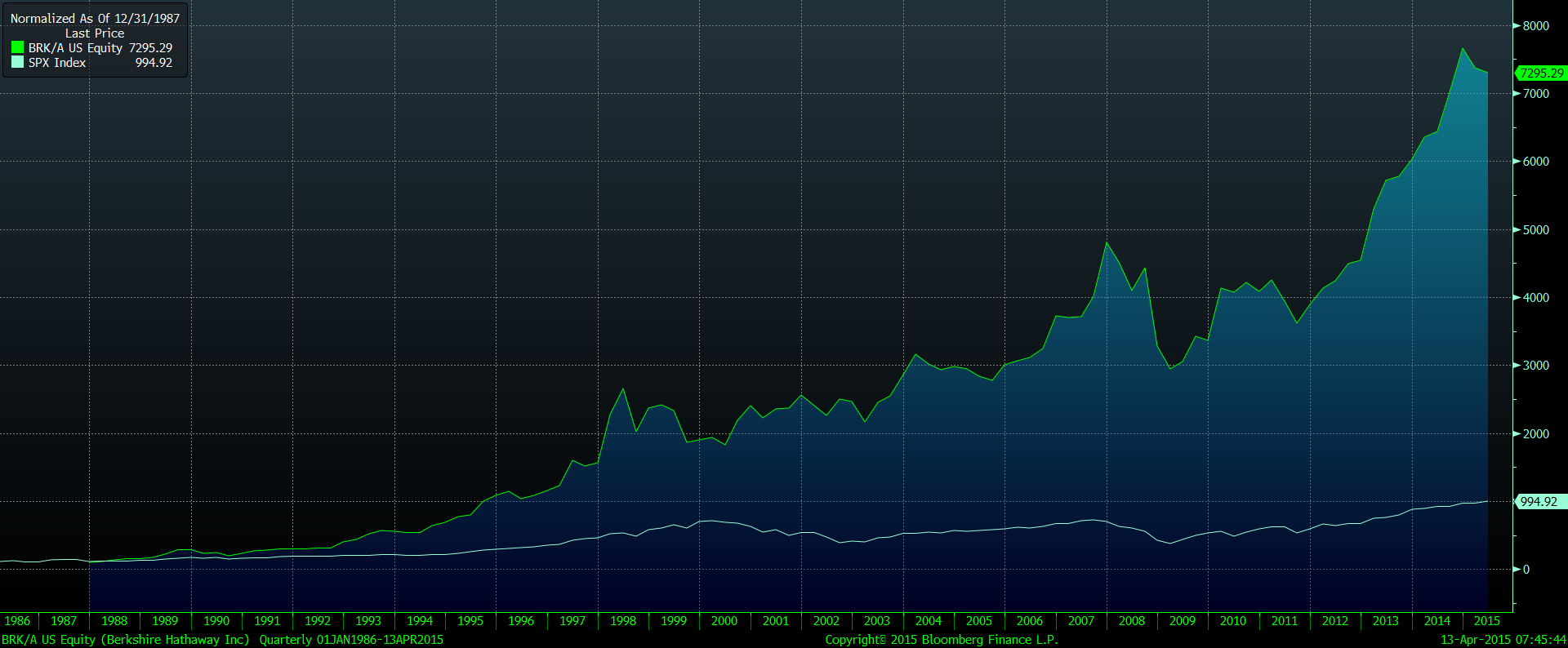

Those investors who take a buy-and-hold (or more appropriately buy-and-watch rather than buy-and-forget) approach to investing should be more interested in a company’s long-range outlook and be less concerned about its near-term performance. In order for companies to deliver the best results, a long-term view is nearly essential. In today’s corporate America, the company that stands out the most for its long-term thinking is Berkshire Hathaway. Warren Buffett, one of history’s most successful investors and a true long-term thinker is Berkshire’s CEO. As can be seen in the chart below, Berkshire has soundly outperformed the S&P 500 Index over the past 30 years.

The question is: What keeps corporate management teams from thinking long term? Unfortunately, CEOs know that any action that negatively impacts the next few quarters’ results can incur investor wrath. This is true even if the actions are likely to add value over time. This causes management to play it safe by spending less on research and development (R&D), lowering capital expenditures (CapEx) or increasing the amount spent to repurchase shares. All of these actions can benefit near-term performance and cause a company’s stock to move higher today. It can also help keep activist investors away.

However, short-term behavior has a cost. According to researchers at Stanford University, the pressure to meet quarterly earnings targets may be causing companies to allocate less to R&D. They estimate this reduction lowers US growth by 0.1% per year. Outside the realm of public companies, the pressures to deliver near-term performance are fewer. Studies have found that privately held companies, which do not have to answer to shareholders, invest at almost 2.5-times the rate of their publicly held industry peers. It is estimated that the weaker investment rate among the largest 350 publicly traded companies in America could be lowering US growth by another 0.2% annually.

It should not take the threat of activist investors to encourage executives to lay out a long-term strategy for value creation. The largest rewards should be earned by those managers who add long-term value and not just a quick pop in the share price. Corporate boards should encourage such behavior. Unfortunately, many CEOs attribute the pressure to focus on the short term to their board members.

At BWFA, we believe an investment time horizon of three-to-five years is the minimum that should be considered for an investment to be classified as long-term. Ideally, an even longer holding period is appropriate. In his book Common Stocks and Uncommon Profits Philip Fisher (one of the greatest investors of all time; his approach also significantly impacted Buffett) stated that “If the job has been correctly done when a common stock is purchased, the time to sell it is almost never.” When reviewing existing portfolio holdings as well as when looking for new investments, we look for signs that management’s thinking is focused on the long term rather than the short term. We tend to shy away from or avoid companies that appear to be chasing growth for the sake of growth, for example, by lowering margins in order to retain business. Ideally, we are hoping to find companies that can be held in client portfolios for many years.