What can the 1918 influenza pandemic, the so-called “Spanish Flu”, teach us about how the markets have responded to current health concerns—and also how to act accordingly?

There has been a “protracted discounting” of the market and the underlying value of the stocks since the highs in mid-February 2020. The stock market once again continues to be an economic leading indicator, anticipating the economic impact that emerged from the widespread business shut down in the wake of the outbreak.

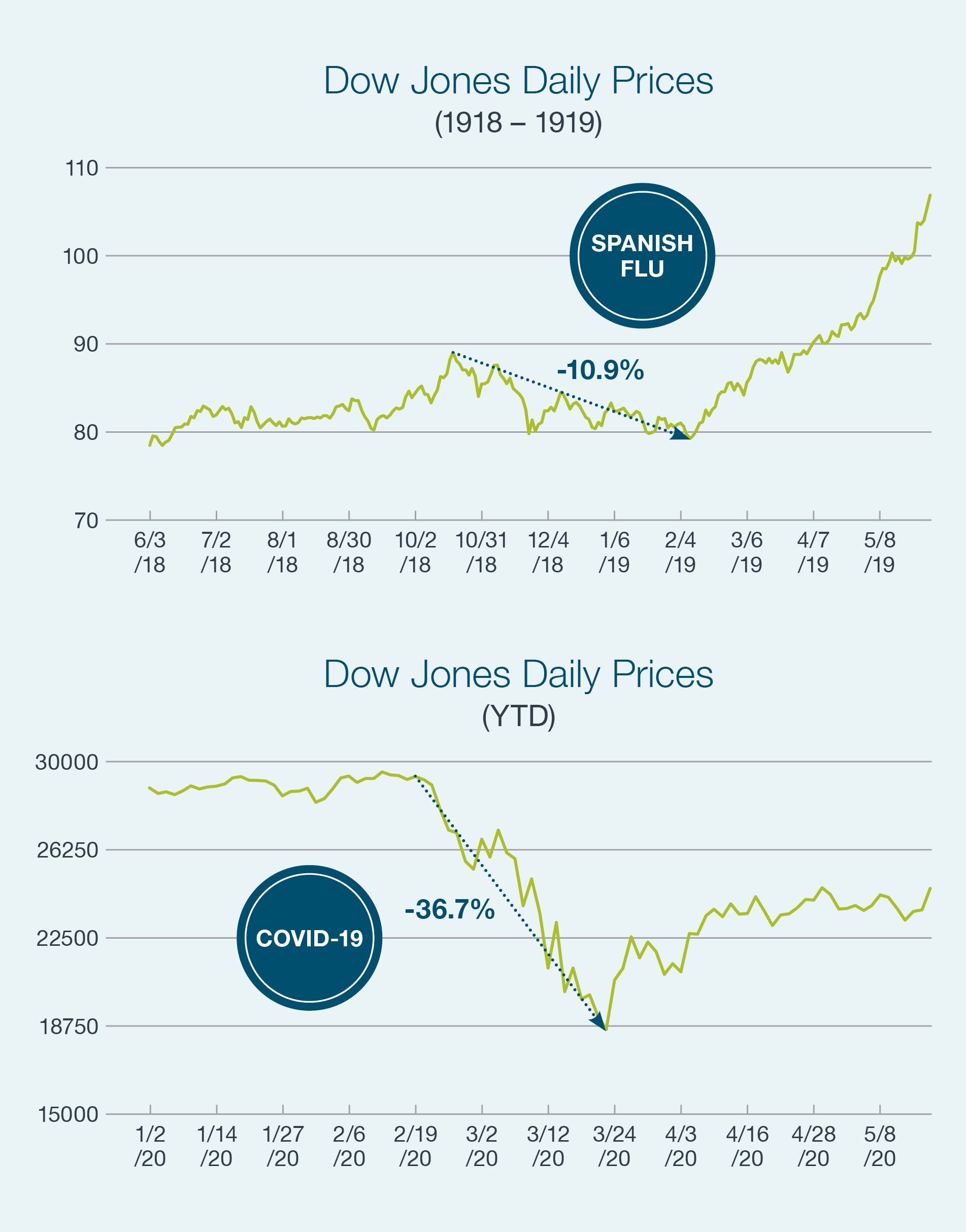

The “protracted discount” of the market from COVID-19, or a loss of over 30% in the US stock market from peak to trough in mid-February 2020, was quickly followed by a sharp recovery. This reminds us of the market reaction of another global pandemic, the Spanish Flu of 1918. While the two are not fully parallel, we can draw some comparisons to frame our thinking about how we react in extreme conditions and approach investing.

As of the writing of this article, we still wonder about potential future waves of additional COVID-19 outbreaks, certainly here in the US, and also worldwide. The Spanish Flu had a few waves — two relatively ”mild“ ones, and a more severe outbreak in the middle, all lasting over a period of about one year total. Even though the mortality rates of the Spanish Flu were many multiples higher than the current number of victims of COVID-19, the stock market in 1918-19 never went into bear market territory, dropping only 11% from peak to trough.

Today, even after a stock market recovery (so far) of 30%+, we are still down more today, post-recovery, than the total downturn of the much more severe Spanish Flu.

Of course, we must be cautious when comparing two events 100 years apart, but it lends some perspective when you see how the market reacted in the past during a more deadly pandemic. The existence of the 24-hour news cycle and computerized institutional trading could account for the more drastic movements in today’s market versus that of 100 years ago. As you can view in the chart of 1918-1919, the market recovered while the Spanish Flu pandemic ran its course (though not without unimaginable suffering and death and worldwide uncertainty).

WHAT DO WE DO NOW? FROM OUR PERSPECTIVE:

- Stay Invested

- Maintain diversification in those investments

- Do not panic or overreact to changes in investments

BWFA portfolios are managed to attempt to take advantage of long term opportunities while weathering the storm of an unprecedented and unexpected event like the COVID-19 crisis.

We invest in diverse areas for growth, appropriately allocated to each client — seeking to determine the “winners and losers” for the future economy while assessing short term risks. During the Spanish Flu, health care businesses fared better than services and entertainment. In today’s stressed economy we see similar trends to 1918 with more options to invest today considering the “stay at home” conditions we have been experiencing.

BWFA portfolios are managed to attempt to take advantage of long term opportunities while weathering the storm of an unprecedented and unexpected event like the COVID-19 crisis.

We balance with non-correlating investments seeking to smooth out volatility where possible (in the first quarter of 2020 pretty much everything went down-and by a large percentage!)

We match long term investments with long term goals and short term investments with short term needs. In many cases, BWFA clients require ongoing withdrawals and they are insulated from the downturns in stocks like we experienced earlier in 2020. Our portfolios are designed so that we are not selling stocks at the worst time just to satisfy these withdrawals.

The financial behemoth Vanguard has performed extensive research studying how investors gauge value from a professional advisor. According to Vanguard, the roles of the advisor can be assessed in these three main categories:

Portfolio value – advisors help clients by maintaining the optimal allocations of stock, income, and cash. This has been shown to be less important than other areas, but still vital for achieving long term results.

Financial value – advisors assist clients in identifying goals and developing a plan to achieve the goals. In addition to investing, this is very essential for client success because it looks more broadly at spending, saving, risk management, and projecting for retirement, among other things.

Emotional value – advisors assist clients in making prudent decisions, particularly during challenging times. This tends to be the biggest component of value — the client trusts and develops a personal connection with the advisor and this builds confidence in the advice and decision-making from the objective fiduciary acting in the clients’ best interests and in accord with their stated goals.

We value our role as advisor to our clients. Our goal is to maintain a consistent philosophy of investing, coupled with our financial planning work, so that clients can successfully achieve lifetime goals!

JOSEPH MANFREDI

MBA

COO, Senior Portfolio Manager & Executive Manager

jmanfredi@bwfa.com