Some employers offer 401(k) plans that allow participants the opportunity to make Roth 401(k) contributions. If you’re lucky enough to work for an employer that offers this option, Roth contributions could play an important role in helping enhance your retirement income.

WHAT IS A ROTH 401(K)?

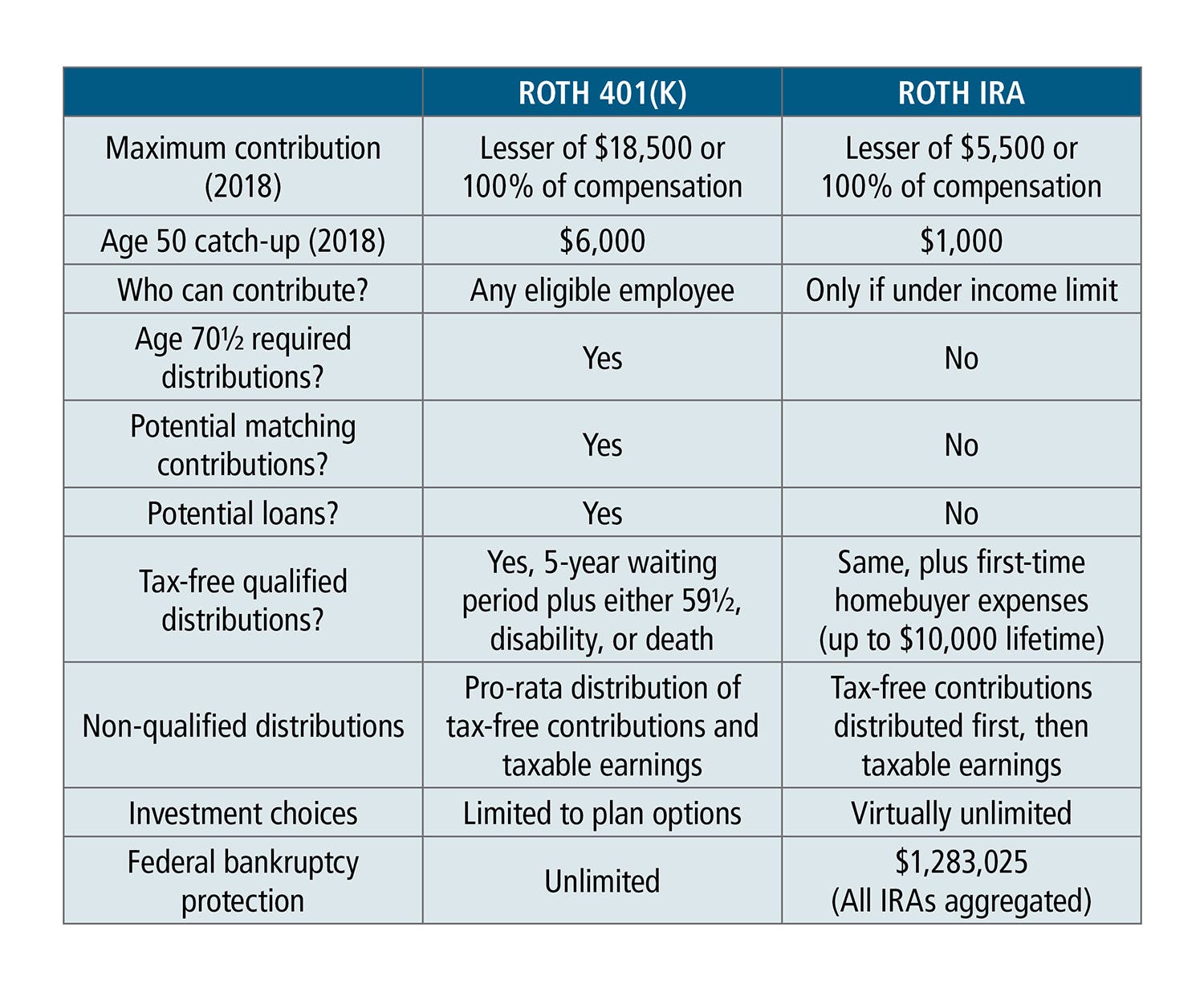

A Roth 401(k) is simply a traditional 401(k) plan that accepts Roth 401(k) contributions. Roth 401(k) contributions are made on an after-tax basis, just like Roth IRA contributions. This means there’s no up-front tax benefit, but if certain conditions are met, your Roth 401(k) contributions and all accumulated investment earnings on those contributions are free from federal income tax when distributed from the plan. (403(b) and 457(b) plans can also allow Roth contributions.)

WHO CAN CONTRIBUTE?

Unlike Roth IRAs, where individuals who earn more than a certain dollar amount aren’t allowed to contribute, you can make Roth contributions, regardless of your salary level, as soon as you’re eligible to participate in the plan. And while a 401(k) plan can require employees to wait up to one year before they become eligible to contribute, many plans allow you to contribute beginning with your first paycheck.

HOW MUCH CAN I CONTRIBUTE?

There’s an overall cap on your combined pre-tax and Roth 401(k) contributions. You can contribute up to $18,500 of your pay ($24,500 if you’re age 50 or older) to a 401(k) plan in 2018. You can split your contribution any way you wish. For example, you can make $10,000 in Roth contributions and $8,500 in pre-tax 401(k) contributions. It’s up to you.

But keep in mind that if you also contribute to another employer’s 401(k), 403(b), SIMPLE, or SAR-SEP plan, your total contributions to all of these plans — both pre-tax and Roth — can’t exceed $18,500 ($24,500 if you’re age 50 or older). It’s up to you to make sure you don’t exceed these limits if you contribute to plans of more than one employer.

CAN I ALSO CONTRIBUTE TO A ROTH IRA?

Yes. Your participation in a Roth 401(k) plan has no impact on your ability to contribute to a Roth IRA. You can contribute to both if you wish (assuming you meet the Roth IRA income limits). You can contribute up to $5,500 to a Roth IRA in 2018, $6,500 if you’re age 50 or older (or, if less, 100% of your taxable compensation).

SHOULD I MAKE PRE-TAX OR ROTH 401(K) CONTRIBUTIONS?

When you make pre-tax 401(k) contributions, you don’t pay current income taxes on those dollars but your contributions and investment earnings are fully taxable when you receive a distribution from the plan. In contrast, Roth 401(k) contributions are subject to income taxes up front, but qualified distributions of your contributions and earnings are entirely free from federal income tax.

Which is the better option depends upon your personal situation. If you think you’ll be in a similar or higher tax bracket when you retire, Roth 401(k) contributions may be more appealing, since you’ll effectively lock in today’s lower tax rates. However, if you think you’ll be in a lower tax bracket when you retire, pre-tax 401(k) contributions may be more appropriate. Your investment horizon and projected investment results are also important factors. Before you take any specific action be sure to consult with your own tax or legal counsel.

ARE DISTRIBUTIONS REALLY TAX FREE?

Because your Roth 401(k) contributions are made on an after-tax basis, they’re always free from federal income tax when distributed from the plan. But the investment earnings on your Roth contributions are tax free only if you meet the requirements for a “qualified distribution.”

In general, a distribution is qualified only if it satisfies both of the following:

- It’s made after the end of a five-year waiting period

- The payment is made after you turn 59½, become disabled, or die

The five-year waiting period for qualified distributions starts with the year you make your first Roth contribution to your employer’s 401(k) plan. For example, if you make your first Roth contribution to the plan in December 2018, then the first year of your five-year waiting period is 2018, and your waiting period ends on December 31, 2022.

But if you change employers and roll over your Roth 401(k) account from your prior employer’s plan to your new employer’s plan (assuming the new plan accepts Roth rollovers), the five-year waiting period starts instead with the year you made your first contribution to the earlier plan.

If your distribution isn’t qualified (for example, you receive a payout before the five-year waiting period has elapsed), the portion of your distribution that represents investment earnings on your Roth contributions will be taxable and will be subject to a 10% early distribution penalty unless you are 59½ or another exception applies.

You can generally avoid taxation by rolling your distribution over into a Roth IRA or into another employer’s Roth 401(k), 403(b), or 457(b) plans, if that plan accepts Roth rollovers. (State income tax treatment of Roth 401(k) contributions may differ from the federal rules.)

WHAT ABOUT EMPLOYER CONTRIBUTIONS?

While employers don’t have to contribute to 401(k) plans, many will match all or part of your contributions. Your employer can match your Roth contributions, your pre-tax contributions, or both.

But your employer contributions are always made on a pre-tax basis, even if they match your Roth contributions. That is, your employer’s contributions, and investment earnings on those contributions, are not taxed until you receive a plan distribution.

WHAT ELSE DO I NEED TO KNOW?

Like pre-tax 401(k) contributions, your Roth 401(k) contributions and investment earnings can be paid from the plan only after you terminate employment, incur a financial hardship, attain age 59½, become disabled, or die.

Also, unlike Roth IRAs, you must begin taking distributions from a Roth 401(k) plan after you reach age 70½ (or in some cases, after you retire). But this isn’t as significant as it might seem, since you can generally roll over your Roth 401(k) dollars (other than RMDs themselves) into a Roth IRA if you don’t need or want the lifetime distributions.

Employers aren’t required to make Roth contributions available in their 401(k) plans. So be sure to ask your employer if they are considering adding this exciting feature to your plan.

Joseph Caputo | CFP® , Chief Information Officer & Associate Portfolio Manager | jcaputo@bwfa.com