Don’t worry, we’ve got you covered. We are going to work our way through a 1040 (individual income tax return) and give the highlights of the tax changes.

The first item on the return that changed is alimony. Starting in 2018, you are no longer required to claim alimony income. This also means that you will no longer receive a deduction for alimony paid.

The other income that was affected by the change in tax law is related to Pass-through Entities. Qualified entities include sole proprietorships, LLCs, partnerships and S-corporations. You can now deduct up to 20% of your income from a pass-through entity. There are limitations, however, so be sure to talk to your tax advisor before you take the deduction.

One deduction that could be taken even if you didn’t itemize, is moving expenses. Before 2018, you were allowed to deduct moving expenses that were related to a job change. The new job was required to be at least 50 miles from where you used to live and where your old job was. This deduction has been removed completely starting in 2018.

The most significant changes to deductions relate to exemptions and the standard deduction. For 2017 and prior, each taxpayer and dependent was allowed an exemption of $4,150. Starting in 2018, there will be no more exemptions. I know this seems like a huge loss, but the government has made up for some of it by increasing the standard deduction. In the past, a single person, or someone filing married filing separately would get a $6,500 deduction. They now get $12,000. Married filing jointly went from $13,000 to $24,000, and Head of Household went from $8,350 to $18,000.

Those of you that itemize instead of taking the standard deduction are probably wondering how this affects you. There are quite a few changes to the itemized deductions as well.

Before 2018, you could take a deduction on Schedule A for the total combination of state and local income taxes (or sales tax), real estate taxes and personal property taxes. Going forward, you can still take that deduction, but it is limited to $10,000.

The next big thing for itemizers is the change to mortgage interest. If you purchased your home on or before December 14, 2017, you can follow the old law of a deduction of mortgage interest on debt up to $1,000,000. If your house was purchased on December 15, 2017 or after, you are limited to debt up to $750,000. The home equity debt interest on debt up to $100,000 is no longer allowed to be deducted, no matter when the loan was taken out.

If you’re starting to worry about charitable contributions, don’t! The deduction is now allowed up to 60% of Adjusted Gross Income (AGI). This was previously only up to 50%. They also increased the allowance of medical expenses. Starting in 2017 (yes, that’s right), medical expenses over 7.5% of AGI can be included. For 2016 and earlier, this was 10%, unless you were over 65, and then it was 7.5%.

The final change to itemized deductions is the Miscellaneous Deductions. This includes casualty and theft losses, unreimbursed employee expenses, tax preparation fees, investment fees, and even safety deposit boxes. These are no longer deductible. This may be a hit for some, but many people never received the benefit for these anyway, because you could only deduct the amount that was over 2% of your AGI.

The most significant changes to deductions relate to exemptions and the standard deduction. For 2017 and prior, each taxpayer and dependent was allowed an exemption of $4,150. Starting in 2018, there will be no more exemptions. I know this seems like a huge loss, but the government has made up for some of it by increasing the standard deduction. In the past, a single person, or someone filing married filing separately would get a $6,500 deduction. They now get $12,000. Married filing jointly went from $13,000 to $24,000, and Head of Household went from $8,350 to $18,000.

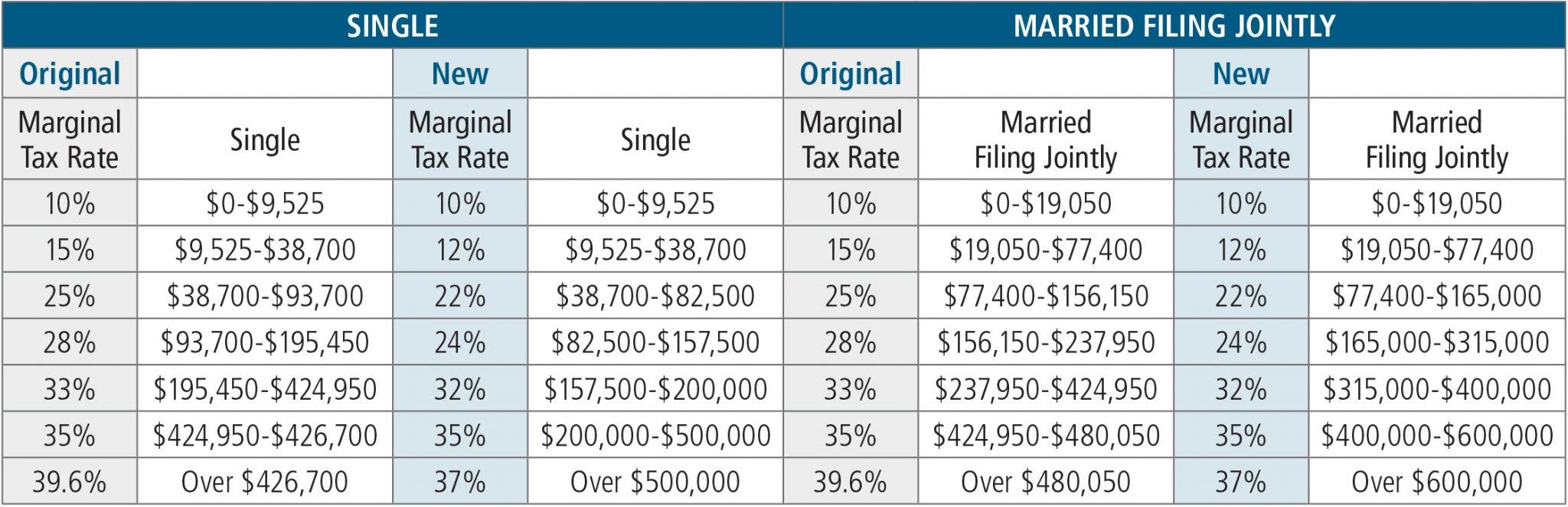

Now that we’ve completely changed our taxable income, let’s talk about the tax rates themselves. Below are comparisons of the Single bracket and the Married Filing Jointly bracket. Keep in mind that these are graduated brackets. Just because your income falls into the 32% tax bracket, it doesn’t mean that all of your income is taxed at 32%. Only the amount over $157,500 is taxed at that rate. Everything below the $157,500 is taxed at each income’s respective bracket.

For those of you that fall into Alternative Minimum Tax (AMT), there are some great changes for you. The original income threshold that put a taxpayer into AMT was $120,700 for a Single taxpayer and $160,900 for Married Filing Jointly. These have now increased to $500,000 and $1,000,000, respectively. The exemptions that are allowed have also increased. Originally, Single or Head of Household was allowed $54,300, Married Filing Jointly was $84,500 and Married Filing separately was $42,250. These have now increased to $70,300, $109,400 and $54,700, respectively. Many of you that once fell into the AMT, have now been pushed back out.

Now that we have your total tax for the year, let’s talk about credits; namely the Child Tax Credit. This credit saw a lot of change in the new tax law. The original credit was set up as follows: Each child under 17 qualified for a $1,000 tax credit. The refundable amount of the credit was up to 15% of earned income. The AGI phase-outs started at Single over $75,000 and Married Filing Jointly over $110,000. Starting in 2018, each child under 17 qualifies for a $2,000 credit. The refundable amount of the credit is $1,400, and the phase-outs have increased to Single over $200,000 and Married Filing Jointly over $400,000. Hopefully that gives a few more people a credit for all of those kids.

Although many states are still deciding how to handle the new tax law changes, there is one already decided, partially state-related change. The 529 College Savings Plan has been in existence since 1996. The way it works is that you contribute to a 529 on behalf of a future/current student. The contribution grows tax-free until the money is needed to pay for college. When the money is distributed and paid to a qualified university, there are no tax implications. If, however, the money is used for something other than tuition, room and board, books or computer equipment, the distribution may be taxable and subject to an early-distribution penalty. There is no deduction for the contribution on your Federal return, but many states allow a limited deduction each year. Maryland in particular allows a deduction of $2,500 per contributor, per beneficiary, per year as long as it is into a Maryland specific 529 plan (which does not mean that the student has to attend a Maryland school). If you happen to “over contribute” in one year, it will carry forward to the next year.

Starting in 2018, these tax-free accounts can now be used for K-12 private schools. The only expenses that are allowed to be paid are tuition and tutoring. Although the amount of a distribution used for a college or university is unlimited, K-12 can only be up to $10,000 a year. Because these contributions are placed into a 529 plan, most states are still allowing the deduction to be taken on the state return. Check with your 529 provider as well as the state you file in to see what they offer.

One final note is related to the increase in the estate and gift tax exemption. Each individual is allowed to gift up to $15,000 (in 2018) to one individual, without having to file a gift tax return. Anything more than the $15,000 will reduce the amount of your lifetime exclusion. This exclusion was originally $5,000,000 per person, but has now been increased to $10,000,000. When your day comes, anything left in your estate will reduce the exclusion to zero, and then the leftover will be taxed at the estate rate.

We hope that this was informative and not too overwhelming. As always, if you have any tax questions, we have an entire tax department waiting for your call.

Rachel Duncan | Tax Advisor | rduncan@bwfa.com