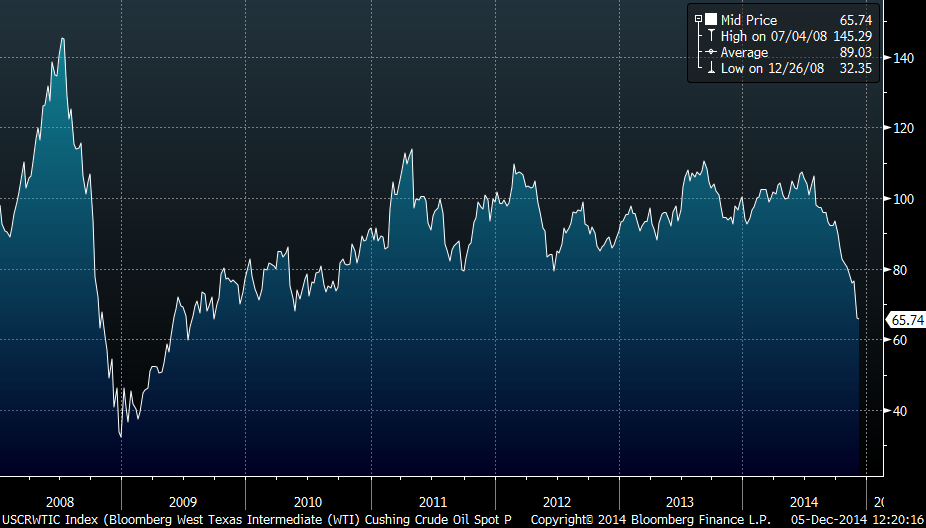

Long-time followers of the oil markets, who are honest with themselves, should readily admit how hard it is to forecast oil prices. Many unpredictable factors can impact oil prices (e.g., geopolitics, foreign currency risk – oil is only priced in dollars). Plus, oil is such a significant factor in the economies of oil-producing nations that the normal laws of supply and demand do not always apply. If one were to review the predictions of those that forecast oil prices, it is extremely unlikely that she would find even one analyst that correctly forecast the path of oil prices depicted in the chart that appears below.

The latest news came on Thanksgiving Day when OPEC announced that it would keep supply at current levels, rather than cut production to try to push prices a bit higher. This action was contrary to OPEC’s historical actions, which have typically focused on defending prices rather than market share. Oil prices, which had already been under pressure prior to this announcement fell even more. Currently, oil prices are at their lowest levels since 2010’s second quarter.

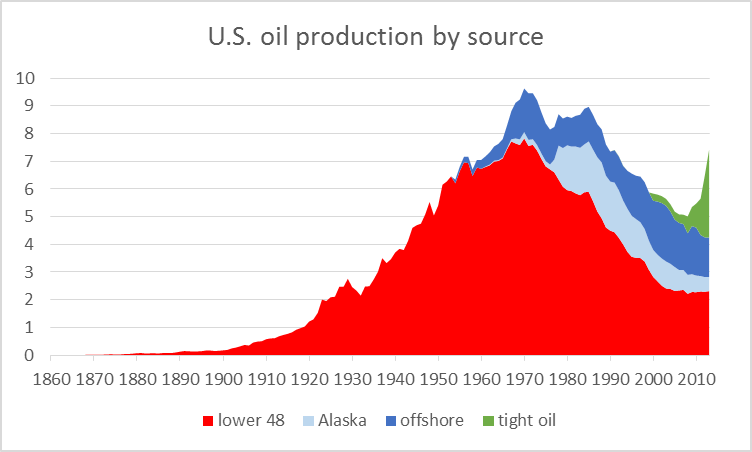

The primary factor that started oil’s downward trend is increased supply. In the U.S., oil production growth has been driven by the fracking of oil trapped in tight geologic formations (Oil Shale). Absent tight oil, U.S. production would have declined by more than one million barrels a day (mb/d) over the last 10 years. It would also have fallen roughly 5.5 mb/d from its 1970 peak. (Note that current production is roughly nine mb/d. The following chart, which shows production of a little more than seven mb/d only includes data through 2013.) In addition to the U.S., production has also increased in Libya.

U.S. field production of crude oil, by source, 1860-2013, in millions of barrels per day. Source: Hamilton (2014).

Higher production is not the only factor behind the oil-price decline. Demand growth has also slowed, especially in emerging markets and Europe. There is also increasing concern that Saudi Arabia is reconsidering its long-term commitment to play a balancing role in world oil markets.

Longer term, we think oil prices are more likely to move higher. Historically, oil demand has grown 1-1.5% annually. While that does not seem like a lot, it is, especially when you consider that a traditional oil field’s production declines about 6% annually. Because of the nature of the extraction process, production from tight oil wells falls at a materially faster pace. As a result, absent investment in new oil projects, supply will fall, putting upward pressure on oil prices. In addition, higher oil prices are needed to make production from tight oil, ultra-deep water, and oil sands projects economic.

We certainly do not pretend that we can accurately predict the near-term direction of oil prices. However, over the long term, we believe that prices will increase. Against this backdrop, we think there are opportunities to add shares of quality companies involved in the production of oil at attractive prices. Many also have an above-average dividend yield. Such securities are particularly attractive for investors who need a mixture of growth and income in their investment portfolios.