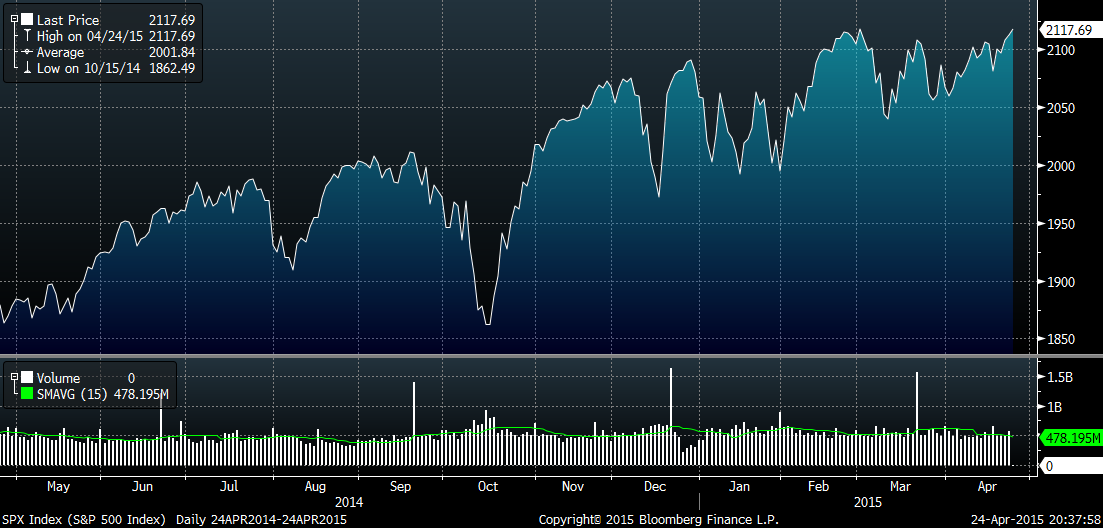

After closing at a record high more than 50 times in 2014, the S&P 500 Index has closed at a new high only six times so far in 2015 – this past Friday was the sixth. In fact, in 2015, the S&P 500 has largely traded within about 5% of the 2000 level. At the same time, it has been nearly 1,300 calendar days since investors last experienced a market correction (generally considered to be a decline of 10% or more from a market top) – this last occurred about 1,300 days ago on October 4, 2011.

We certainly do not expect the market to march consistently higher. While we do not know if or when the market will correct, corrections are healthy and bear markets (a decline of 20% or more) are to be expected from time-to-time. At the same time, the market has more or less meandered for much of 2015, trading in a relatively narrow range – the S&P 500’s year-to-date low of 1992 was reached on January 15 and its record-high close 2117 was set on March 2). It is almost as if the market is waiting for a catalyst that will cause it to break out from this range.

There are a number of possible explanations for the market’s behavior over the past few months. First, stocks no longer appear as cheap as they once were. Based on information provided by Yardeni Research, the forward price-to earnings ratio (P/E) of the S&P 500 is about 17. In March, the median forward P/E for the S&P 500 was 17.5, exceeding the composite’s 16.9 reading on a market-capitalization basis. These levels are high by historical standards. Anecdotally, we also note that we are finding it increasingly difficult to find stocks we consider cheap in the present environment.

There are two factors that are negatively impacting analyst’s earnings forecasts. The first is the continued weakness in oil prices. Earnings estimates for energy companies continue to tumble. Second is the strength of the U.S. dollar. The stronger dollar reduces the value of revenues generated in foreign currencies such as the euro or the Brazilian real when those amounts are converted back into dollars. This dynamic has hurt results for a number of companies that have already reported first quarter results. For example, companies such as General Motors Co., General Electric Co., Facebook Inc. and Coca-Cola have posted year-over-year revenue declines that their management teams largely attributed to the stronger dollar. The dollar is currently expected to remain strong this year, and many companies have lowered their full-year outlook as well.

The market’s apparent lack of direction can at least partially be attributed to factors such as those just cited. One day the market may seem primed to decline based on futures trading, only to move higher for the day. The next day may see the exact opposite happen. The market may even change course mid-day.

If the market does correct, investors with a long-term perspective are typically best to stay invested. Selling shares necessitates the payment of taxes on any gains. Plus, there are no assurances that such investors will be able to buy back in at a lower price in the future. It is typically better to stay invested for the long term rather than try and time the market.

Against this uncertain backdrop, we maintain our positive long-term outlook. We remain true to our investment process and are patiently looking for the best opportunities the market has to offer. We also believe our long-term approach offers additional advantages. At times, impatient investors can push the price of good stocks lower. This can provide the opportunity to add high-quality equities at even better prices.