If one only looks at the overall year-to-date change in the S&P 500 Index (+1.2%), he or she might think there has not been much change to the broader market landscape. However, by digging deeper, one will note changes in market leadership from both a sector and market capitalization perspective.

In 2013, the sector delivering the biggest gains was Consumer Discretionary (+43.1%) and the fourth-largest gains were delivered by Financials stocks (+35.6%). Year-to-date, the returns of Consumer Discretionary (-4.7%) and Financials (-0.7%) stocks lag all other sectors within the S&P 500. On the other hand, in 2013, Energy (+25.1%) and Utilities (+13.2%) were the second- and third-worst performers in the Index. Their relative performance has changed this year as Utilities (+10.3%) and Energy (+4.5%) have provided the best returns of any sectors within the S&P 500.

On Tuesday May 13, the S&P 500 and Dow Industrials reached new all-time highs. According to work published by Argus Research, the returns of these benchmarks have been driven by the largest 200 U.S. companies. In contrast, the Nasdaq Composite, which is more technology heavy, has fallen 6.6% from its mid-March high and is down 2.5% year-to-date.

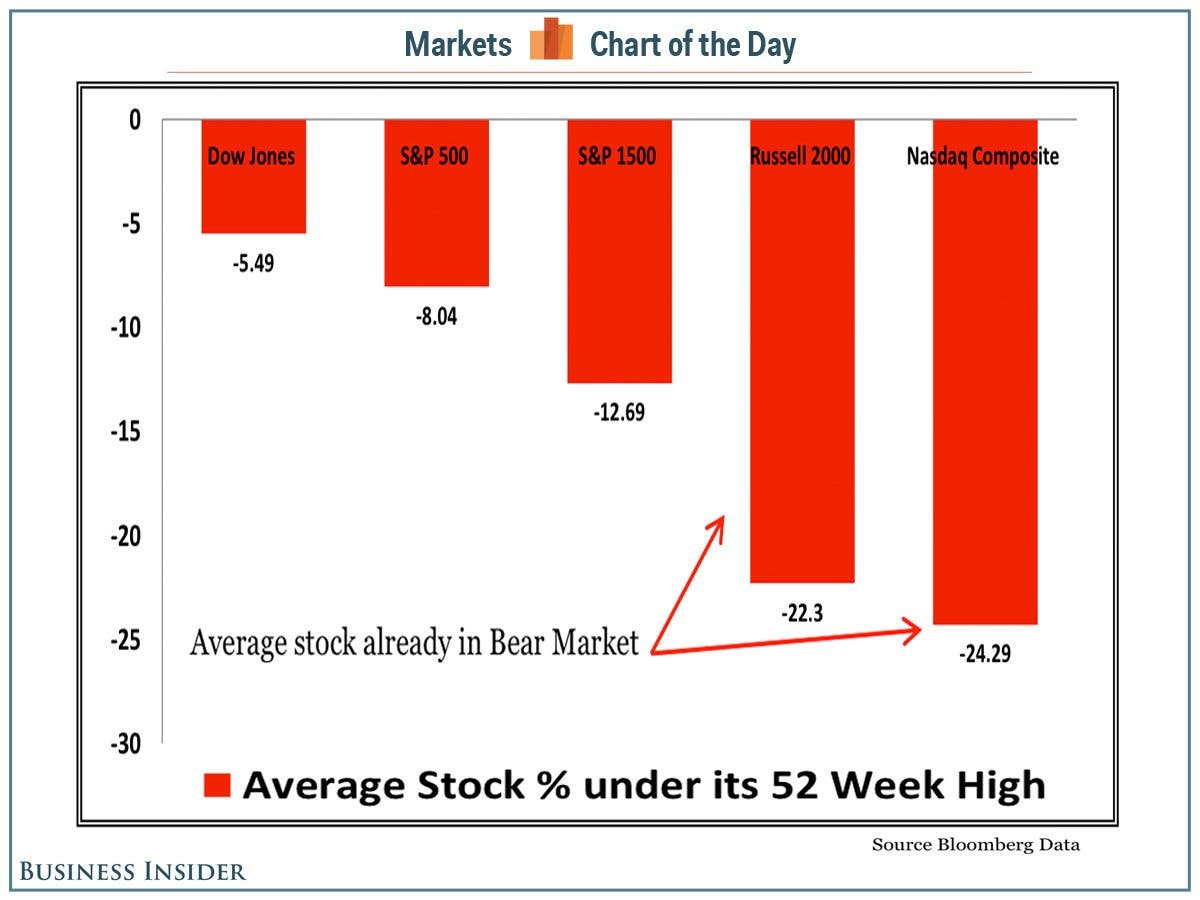

Indexes and sector performance only tell us how broad swaths of the market are performing. By digging deeper, one can get a better idea of how the market leadership is changing. Research by FBN Securities, provides further evidence that large stocks are supporting the large-cap indexes. The Russell 2000, which includes U.S. stocks ranking from 1,001-3,000 in terms of total market capitalization, is down roughly 5.7% year-to-date. According to FBN, as of May 8, the average stock in the Russell 2000 was 22.3% below its 52-week high. On that same date, that index had declined 10.5% from its 52-week high.

Of course, the bigger question is “What does this data mean?” The short answer is no one knows for sure. Typically, a 20% decline is viewed as a sign of a bear market. When sectors such as utilities and large-cap stocks are leading performance, it can indicate that investors are becoming more “defensive” and that the market’s advance is in its later stages. Only time will tell if that is the case.

BWFA Investing Approach

At BWFA, we maintain our long-term positive view of the market. Our year-to-date performance is roughly inline with the broader market averages. In our opinion, recent declines in certain market sectors or groups provide the opportunity to acquire some high-quality stocks at attractive prices. At the same time, it is important that we continue to exercise care and diligence in our research process as we hope to avoid acquiring stocks that represent value “traps” rather than securities available at a discounted price.