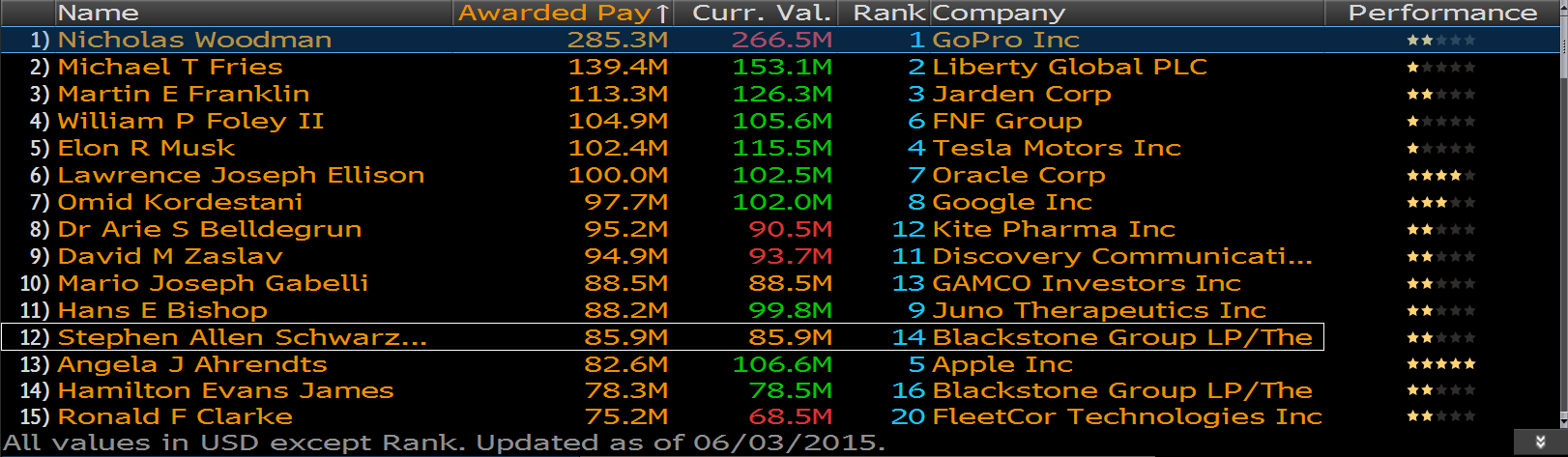

The pay earned by corporate executives has risen rapidly in the last 25 years. According to data provided by Bloomberg, GoPro founder Nicholas Woodman, who earned $285.3 million last year, is currently the top paid executive. (In the chart that follows, the amount in the Curr. Val. column is calculated daily and fluctuates with stock prices. The Awarded Pay amount corresponds to what the executive committee intended to pay the executive for the year.)

Source: Bloomberg

In introductory accounting courses, students are often told that a corporation’s purpose is to “maximize shareholder value.” A 1981 speech by former General Electric CEO Jack Welch titled “Growing Fast in a Slow-Growth Economy” is often acknowledged as the “dawn” of the obsession with shareholder value. The idea’s roots can be traced to an editorial by Milton Friedman in 1970, in which he wrote, “There is one and only one social responsibility of business – to use its resources and engage in activities designed to increase its profits…”

In theory, the premise that the corporation exists for the shareholder appears sound. Shareholders benefit from a corporation’s success through a higher share price as well as dividends. In fact, there was a time when the primary reason that people decided to purchase equity shares was for the dividend yield. The possibility that the share price might increase was only a secondary consideration.

Over time, corporations have become more focused on generating profits to the exclusion of all else. While this was happening, stock options became a more significant part of managerial compensation. The combination of these elements was based on the idea that managers should have a stake in the corporation, meaning the interests of managers and shareholders would be better aligned.

The way corporations are managed has also changed. Share price has become the primary focus, causing dividends to fall in importance. In many cases, share repurchases have become a substitute for dividends. Corporations seem to be more focused on short-term thinking and obsessively focusing on those actions that can boost stock prices in the near term.

More recently, the cry against the shareholder value movement has gotten louder. James Montier of GMO UK Ltd. issued a white paper late last year calling Shareholder Value Maximization “The World’s Dumbest Idea.”

Most stock option plans award option holders if a company’s share price rises. However, over time, the market trends higher. It is hard to separate how much of a stock’s rise is unique to the company and how much is attributable to “a rising tide lifting all boats.” It would make more sense to reward managers for outperforming the market. It is also important to note that being the CEO of a major corporation should result in a pretty lucrative payday. Why do managers need even more incentive to do the job they are already well paid to do?

Last week’s commentary discussed “special charges” that companies would like analysts to exclude from their earnings. Some companies exclude stock-based compensation from GAAP-based earnings because they are non-cash amounts. However, when an employee exercises stock options, the company issues new stock to cover them. As a result, stock options inherently dilute the shares of existing shareholders, making them worth less. In our view, stock compensation expense should not be excluded from results. It represents a form of compensation and should be counted.

When reviewing companies that are held or that could be added to client portfolios, BWFA reviews compensation and the use of stock options. Compensating employees is one way that capital is allocated. Effective capital allocation is an important element of our stock selection process.