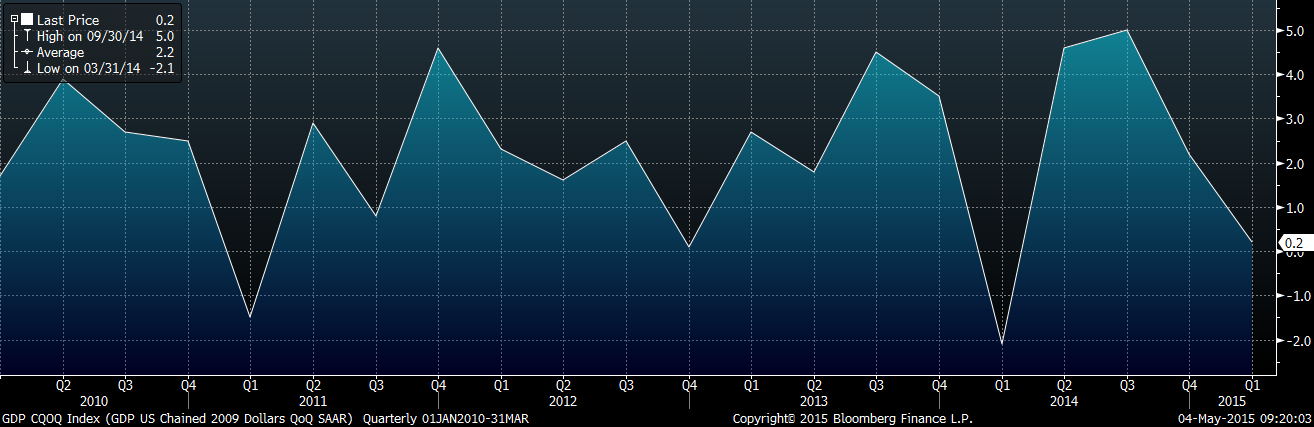

Last Wednesday, we learned that the U.S. economy grew at a relatively anemic 0.2% annualized rate in the first quarter. This was a sharp decline from the prior quarter when gross domestic product (GDP) grew by 2.2%. It was the weakest performance since 2014’s first three months when GDP contracted year-over-year.

The pattern of weak first-quarter data should not have been unexpected. As shown below, it has been the case for most of the last five years. From 2010-2014, average first quarter GDP has been just 0.6%, significantly lower than the 2.9% average for all other quarters. That has equated to moderate overall expansion but no sustained breakout for the economy.

After economic data such as quarterly GDP is reported, numerous articles can be found discussing the figures as well as what they might mean. Similarly, the financial news networks interview numerous market pundits soliciting opinions about the data.

While such data is interesting, as a general rule, it does not materially impact our long-term investment decisions. Forecasting economic growth is also not an important element of our investment process. We know we are not alone in our view. At this past Saturday’s shareholder meeting, Warren Buffett said the following;

“Any company that has one economist has one employee too many.”

Some might be surprised by this view. However, it is important to remember that the stock market is not the economy. For example, in a recent article, Larry Swedroe showed how China and the US demonstrate this disconnect. He found that over the five-year period from 2010-2014, economic growth in China averaged 8.5% – more than four times as fast as the US’s growth rate of just under 2%. While you might think that this would equate to an opportune time to invest in China; it was not. During this period, Chinese stocks (as measured by the most popular China ETF: FXI) grew by only 1.7% annually. This is in sharp contrast to the 15.3% annualized growth investors in US stocks realized over the same period (as measured by an ETF tracking the S&P 500: SPY).

During this same period, the growth rates of economies of the US and UK were around 2%. However, UK equity investors earned 6.3% annually (as measured by an ETF intended to capture the performance of the UK market: EWU), easily lagging the SPY’s gain.

It is unlikely that the results over this five-year period represent a one-time event. According to the Economist, a study by professors at the London Business School found that dating back to 1900, there was actually an inverse relationship between GDP growth per capita and investment returns.

In an effort to evaluate how country growth compared to following year investment returns, they also divided countries into groups based on GDP growth over the previous five years. They found that over the next year the market in high-growth countries grew 6%; it grew by 12% in low-growth countries. The report “found no statistical link between one year’s GDP growth rate and the next year’s investment returns.”

What might be behind such apparently surprising results? The markets in countries with higher growth rates tend to be expensive. Optimism about a country’s future growth prospects likely pushes equity prices higher.

The most important takeaway is that value matters. It is best to buy low and sell high. As a general rule, the higher the price-earnings ratio is when you buy a stock or a market index, the lower the return is likely to be over the next five-to-ten years. Valuation is a key part of BWFA’s investment process.